In 2024, most of the automotive headlines were once again focused on the used car market. High interest rates and inflation caused a dip in consumer purchasing power, leading to a decline in demand for mid-range used vehicles. However, the lower end of the market, including salvage and auctioned cars, remained relatively stable as budget-conscious buyers sought affordable options. The markets and metals market experienced some notable fluctuations over the last 365 days but for the most part remained mostly stable..

As with past Wreckonomics coverage, much of this is not new information or proprietary to ARS, but it should present a unique assembly of ideas. The insights presented here are supported by the Wreckonomics YIR Resource Document and slides available below.

So let’s breakdown the Wreckonomics landscape for 2024:

Macro-Economic Minute (slides 7-11)

The used car market continued to fluctuate throughout 2024. Additionally, the rising costs of maintenance, repairs, and operations continued to affect vehicle owners, fleets, and insurance companies. Qualified repair technicians remained scarce, further complicating future cost projections. When combined, these external pressures resulted in interesting outcomes for our low-value segment.

Transportation & Vehicles in Operation (slides 12-14)

In 2024, the number of vehicles in operation (VIO) reached another record high. New Car sales had a strong sales year.

High new car prices and financing costs pinched owners but didn’t destroy sales figures. Due in part to economic uncertainty, older vehicles remained on the road longer. This extended lifespan also increased demand for replacement parts, providing a boost to the salvage and recycling industry.

Overall Americans continued their amazing migrations and movements. Vehicle miles travelled grew again with air and rail travel.

Electric Vehicles & Salvage Value Trends

Electric vehicles (EVs) grew as a segment of VIO and correspondingly, more electric cars entering auctions at wholesale. Battery replacement costs, combined with repair complexities, still present challenges, but 2024 saw an increased demand for EV parts such as lithium-ion batteries and copper. That said, few expect the numbers to continue so positively in an age of tariffs Lastly, Americans still love the internal combustion engine, and traditional vehicles continue to account for the majority of new car purchases.

Sustainability remained a top priority in 2024, with stricter environmental regulations and increased consumer awareness being the drivers of innovation in vehicle recycling. More scrapyards and auto recyclers implemented eco-friendly dismantling processes, improving efficiency and reducing landfill waste. However the easing of environmental regulations will have a lasting effect in the years to come.

Supply (slides 15-20)

As mentioned previously, Vehicles in Operation (VIO) rose again last year to over 291 million units. This continued a 50 year trend for VIO. However there are some interesting forces that are influencing our low end segment and our auto recycling appetites.

However, VIO doesn’t provide the full picture of supply. On a more positive note, vehicle scrappage rates remained mostly consistent with the last five years of averages.. This suggests that the ‘retention pressures’ in the auto sector have not only eased, but that American owners might not be holding onto their vehicles as long as we previously thought. This is largely due to the rising expenses of auto maintenance and repair. From 2023 to 2024, vehicle repair costs increased by 4.3% annually, marking a total rise of nearly 55% over the course of the last 10 years. These steep increases have made maintaining older vehicles significantly more expensive for the average American.

The increasing availability of salvage units is also obstructed by the increased value of vehicles resulting in lower total loss ratios.

Values & Wholesale (slides 21-23)

While the wholesale supply has stabilized and is expected to be strong for years to come, vehicle values are still very much in flux. Wholesale closed the year down 7% year over year but still way up over pre pandemic numbers. It’s interesting to note that wholesale has given up over 50% of the pandemic rapid gains in the market but still spectacularly above 2020 values.

Unique to our services, ARS tracks the market on low end vehicles on a daily basis. We pull wholesale market data on high mileage, high year, low ACV units and use a mix of our own data and observed activity to produce an index that helps us work with our clients to make remarketing and channel decisions in real time. Our ARS Low Value Index sees a more significant relapse to pre pandemic values based on auction performance of similar assets. This is attributable to several things including the appetite for low value assets becoming more specific as competition wanes and also the influence of much higher acquisition fees to our recycling partners.

Scrap Performance (slides 24-28)

For our Recycling partners we maintain data related to scrap values, core demand and rare metals collected from end of life vehicles. We update these forces in our Markets & Metals series. In 2024, the market was surprisingly stable overall, the price performances for aluminum, rhodium, palladium and other metals maintained some form of economic security. Copper experienced the most fluctuations, largely being due to the rise in EVs being produced nationwide.

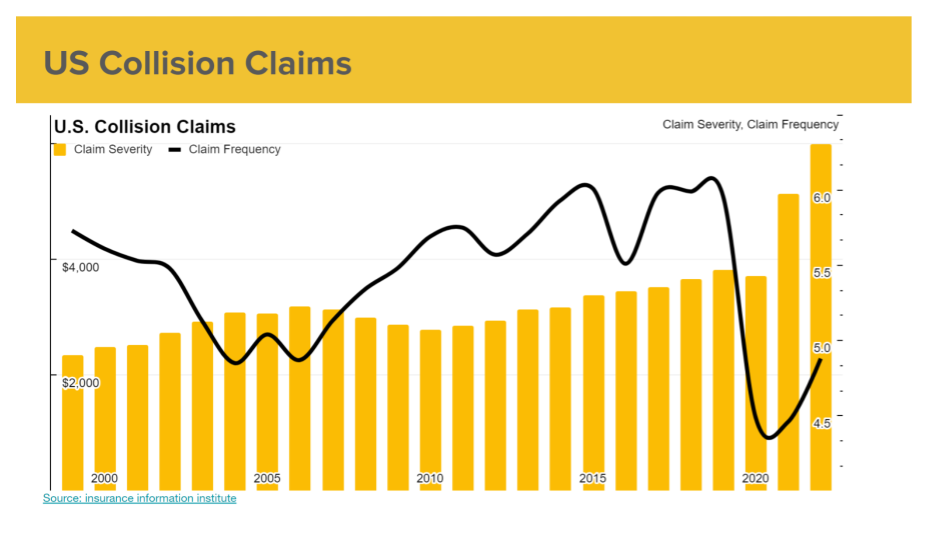

The number of reported collisions in 2024 remained consistent with previous years, with urban congestion and severe weather contributing to accident rates. Many advances in vehicle safety technology have helped reduce fatal crashes, but the rising costs of repairs resulted in more damaged vehicles being deemed ‘total losses’ by insurers. As predicted, 2024 experienced a push in auto insurance rates. This led to a steady influx of salvage vehicles entering auctions, further fueling demand for recycled auto parts and contributing to industry growth.

Metal Prices & Acquisition Costs

The global metals market experienced many fluctuations in 2024. Most recently, steel prices seeing moderate growth early in 2024 before stabilizing. This directly impacted vehicle scrap values, as scrap yards adjusted their payouts based on material costs. We also saw materials that are crucial for EV components, such as copper and aluminum, experience sustained demand, reinforcing the importance of recycling in the automotive sector. In 2024 alone, the price of copper rose 7.7%, largely due to the monumental shift towards EVs. 5 years after the pandemic, market tensions continue to ease, which allows the systems to return to a more domestic appetite.

The recovery and demand form specific automotive metals continues to evolve. Steel remains the most abundant metal in vehicles, with robust recycling demand despite looming tariff challenges. Aluminum is increasingly prized for its lightweight properties, which are essential for enhancing fuel efficiency and improving EV performance. Precious metals such as rhodium, platinum, and palladium (vital components in catalytic converters) are experiencing volatile yet significant demand. Rhodium, due to its rarity and strict emissions standards, commands high prices ($4,637/oz), while platinum and palladium maintain steady recovery rates from scrapped vehicles, underscoring their importance in emission control systems.

Partners purchasing through ARS have been largely protected from this escalation in fees. Sellers on our mBid platform continue to see a much higher recovery ratio for vehicles sold by ARS.

Outlooks for 2025: Thrive vs. Survive (slides 38-40)

Looking ahead, we anticipate further shifts in the salvage market, especially as EV adoption continues to rise and new government policies impact vehicle recycling standards. Advances in AI powered vehicle assessments and online auction platforms will also play a role in shaping the industry’s future.

Additionally, new tariff concerns are expected to influence the automotive recycling sector. Potential trade restrictions on imported vehicle parts and raw materials could impact pricing structures for salvaged and recycled components. Industry players will need to navigate these economic factors carefully to maintain profitability and sustainability.

One key area to watch is the potential for new steel tariffs. Projected to be implemented in mid-March, these tariffs could directly impact the cost of recycled materials. If tariffs drive up steel prices, scrap yards and recyclers may see increased profitability on salvaged metals but could also face higher costs for processing and distribution. The ripple effect couple influence the availability of affordable replacement parts and reshape pricing models across the industry.

With markets going back to pre-pandemic levels and the cost of maintenance expected to stay high due to a continuing shortage of qualified mechanics, we can predict 2025 will be another solid year for vehicle retirement.

Stay tuned for more insights in the coming year as Wreckonomics continues to evolve with the automotive industry’s ever-changing landscape.

To meet the growing retirement needs, ARS spent the last year working closely with our partners in the Automotive Recycling Sector to launch the SHiFT National Vehicle Retirement Initiative. The Nation’s most environmentally friendly auto recycling program. SHiFT enables consumers, fleets, lenders, insurance companies and enterprises the ability to participate in the auto recycling process with measurable environmental benefits. You can learn more about SHiFT Here or reach out to ARS for more information.

If you have a pool of low value vehicles in your portfolio or if you’re looking at ways to maximize recoveries, please reach out to us at ARS. Send us an email; success@arscars.com

STAY IN THE CONVERSATION

Visit ARS Wreckonomics blog:

https://www.arscars.com/category/wreckonomics/

And subscribe for updates

*NOTE: All figures are believed to be reliable and represent approximate pricing based on information obtained prior to publication. Data is sourced from American Recycler, London Metal Exchange, iScrap App, and Scrap Monster. Advanced Remarketing Services is not responsible for the accuracy or completeness of the information provided, or for the use or application of information herein.